Get a Home Equity Line of Credit with a Bad Credit Score

At a Glance

A home equity line of credit, or HELOC, is a revolving line of credit that works like a credit card. The best part: you don’t need good credit to get one. Below we’ll break down the pros and cons of HELOCs, the difference between HELOCs and home equity loans, and more.

In this article, you’ll learn:

What is a HELOC?

A HELOC provides you with a line of credit based on the value of your home, so you can borrow what you need when you need it, and repay the funds over time. In addition to a credit limit, HELOCs usually have a “draw period,” or a set amount of time when you can draw funds from your account.

Because your home’s equity acts as collateral, a HELOC is a secured loan. In other words, you risk losing your home if you default.

Pros

- Can qualify for one even with a fair or poor credit score

- Only borrow what you need

- Many HELOCs don’t have fees

- Flexible repayment options

- Interest on HELOCs can be tax deductible if used to make improvements to your home

- Payments during the draw period are often interest-only, which helps keep monthly payments down

- Some lenders let you lock in a rate during the draw period to avoid fluctuation

Cons

- Variable interest rate at the mercy of the market

- Need considerable equity to qualify

- Need to pay any remaining debt from a HELOC if you sell your home

- Two mortgage payments instead of one

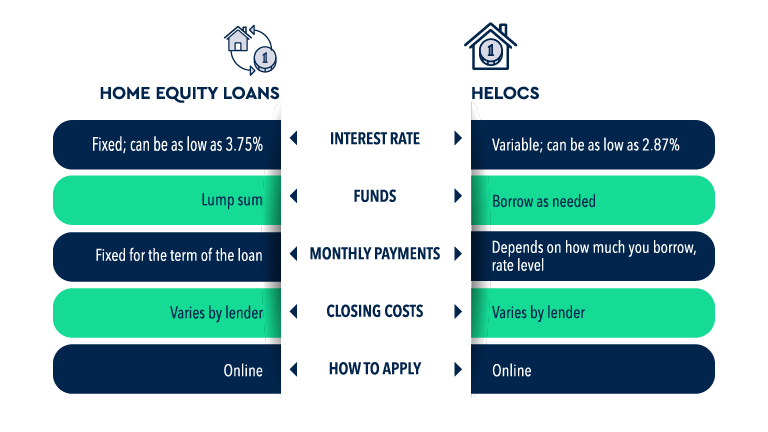

HELOC vs. Home Equity Loan

Home equity loans are a type of second mortgage where you receive a lump sum of cash upfront. These loans have fixed interest rates and fixed monthly payments. Because you’re borrowing against the value of your property, a home equity loan can be easier to get if you have bad credit.

HELOCs, on the other hand, function more like credit cards. You can borrow up to a specific limit of your home equity and repay the debt over time.

What is a bad credit score for a HELOC?

A bad credit score for a HELOC isn’t necessarily the same as a traditional bad credit score. As with other loans, the higher your credit score, the more likely you are to be approved and receive better terms.

The requirements vary by lender, but a FICO credit score of 620 is typically the lowest to get approved for a traditional first mortgage.1 A score this low can make it tricky to get approved for a HELOC. You’ll need a lower debt-to-income ratio, you won’t be able to borrow as much equity, and you’ll have a higher interest rate.

Having a FICO credit score of at least 700 generally gives you a good chance of qualifying for a HELOC at the maximum amount. But you still won’t necessarily get the best rates. The best rates and terms possible typically go to those with credit scores of 760 or higher.

Things to know about HELOCs with bad credit

If you’re approved for a HELOC despite having bad credit, there are some factors you should keep in mind.

Higher interest rates

The worse your credit score is, the higher your interest rate is likely to be because you can be considered a risky borrower. With a higher interest rate, you’re going to be paying a lot more over time.

Changing terms

If your financial situation changes dramatically, your lender can change the terms of your loan. Depending on what’s been contractually agreed to, the lender can freeze or reduce your credit line. This could potentially leave you with less money to borrow than you originally anticipated.

Risking home as collateral

With your home as collateral, missing payments can jeopardize your living situation. If you’re unable to make payments for any reason, the lender can potentially foreclose on your home.

What are the alternatives to HELOCs?

Home equity loans are just one alternative to HELOCs, but there are others.

1. Unsecured personal loans

Unsecured personal loans are based mostly on your creditworthiness. If you have a fair or poor credit score, it may be more difficult to get an unsecured loan. Though you’ll have a higher interest rate and lower loan limit, you won’t risk losing an asset with a missed payment.

Compare: Best Debt Consolidation Loans

2. Balance transfer credit cards

Another option to consolidate debt is to look into a balance transfer credit card. This is usually an option if you want to move a credit card balance from a high-interest card to one with a lower interest rate. Many credit card issuers offer a 0% introductory annual percentage rate (APR) for a set period of time. This method of debt consolidation can help you pay off your debt more quickly.

3.Contact creditors

Explain your situation and why you’re having difficulty making payments to your creditors if you need to. It’s possible to come to a payment agreement that’s more manageable for you.

Home equity loans for bad creditCompare home equity loan lenders

Personal loans for bad creditCompare personal loan lenders

Balance transfer recommendationsCompare balance transfer cards