Planning to Borrow from your 401(k)? Here’s What to Know

At a Glance

Carrying too much debt is a problem that can affect you in several other areas of life. At first glance, using funds from your 401(k) plan to pay off that debt may seem like a good idea, particularly if you have high-interest credit cards. It’s your money. Why not use it? That’s the question we’ll attempt to answer for you today. Here’s what we’ll cover:

What is a 401(k) loan?

A 401(k) loan allows you to borrow money from your retirement savings and pay it back to yourself over time, plus interest. You can typically borrow up to 50% of your balance for up to five years, for a maximum of $50,000.

The interest rate is typically the current prime rate plus 1%. Once you sign the paperwork, you’ll have access to the funds within a few days. Then, the loan payments and the interest get paid back into your account.

Not every plan lets you do this, and how much you’re able to borrow, how often, and repayment terms are dependent on what your employer’s plan allows. The plan may also have rules on a maximum number of loans you may have outstanding on your plan. Note that if you leave your current job, you may have to repay the loan in full very quickly. Or, if you default, you’ll owe both taxes and a penalty if you’re under age 59 ½-years-old.

Should you use a 401(k) loan to pay off debt?

There are a number of reasons you may consider borrowing from your 401(k), including to pay off debt. If you have high-interest debt, such as credit card debt, consolidating it with a 401(k) loan can lower your overall interest rate and simplify your payments:

1. Lower interest rates: The interest rate on a 401(k) loan is typically lower than that of credit cards or other high-interest debt, potentially saving you money on interest payments.

2. No credit check: Since you’re borrowing from your own retirement savings, there’s no need for a credit check, making it easier to qualify for a 401(k) loan than other types of loans.

3. Interest goes back to you: The interest you pay on the loan goes back into your own 401(k) account, essentially making it a self-borrowing option.

4. Quick access to funds: Unlike traditional loans, which may take time to process, you can usually get a 401(k) loan quickly, providing immediate access to funds.

In addition to paying off debt, some other scenarios when it may make sense to take out a 401(k) loan include:

1. Emergency expenses: If you’re facing a financial emergency and have no other means to cover the costs, a 401(k) loan can provide quick access to funds without penalties or taxes (as long as you repay it on time).

2. Home purchase: Some 401(k) plans allow you to use the loan for a down payment on a home, which can help you avoid costly private mortgage insurance (PMI).

3. Cash flow needs: If you need short-term cash flow for a specific purpose, such as starting a business, a 401(k) loan can provide the necessary funds.

It’s best practice to first explore other options for debt repayment, but if those are ruled out, a 401(k) loan might be an acceptable choice.

Alternatives to a 401(k) loan

When considering your financial situation and needs, a 401(k) loan may be an option. However, there are other alternatives that should be considered as well:

Negotiate your interest rate

Before taking out a 401(k) loan, consider negotiating your interest rate on your current debt. This can be a helpful strategy for reducing how much you owe and making your debt more manageable. Here are some steps you can take to negotiate a lower interest rate:

1. Understand your current rates: Know the interest rates you’re currently paying on your debts, such as credit cards, loans, and lines of credit.

2. Research competitive rates: Research current interest rates for similar financial products to understand the market rates and use them as a benchmark for negotiation.

3. Contact your creditors: Call your creditors directly and explain that you’re interested in lowering your interest rate. Be polite and persistent. Mention your good payment history and inquire about any available promotional rates or programs.

If negotiating on your own is challenging, consider seeking help from a credit counseling agency or a debt settlement company. They can negotiate on your behalf and help you develop a plan to manage your debt.

Personal loans

Personal loans are a type of loan you can borrow from a bank, credit union, or online lender. Loan funds can be used for just about any reason, making them a good option for well-qualified borrowers who need financing. Terms and interest rates vary based on lender, your credit score and history, and other factors, but borrowers with good to excellent credit typically qualify for lower interest rates.

These loans are usually unsecured, meaning they don’t have to be backed by collateral, and have fixed terms and rates, so you can quickly and easily calculate your monthly payments, how much the loan will cost over time, and when you’ll have it paid off.

Give yourself options

![]() Use the filters below to refine your search

Use the filters below to refine your search![]()

Sorry, we didn’t find any options that meet your requirements. Please try modifying your preferences.

Congratulations! You’re close to seeing your offers!

Please take a second to review the details you shared earlier

Balance transfer credit cards

You can use a balance transfer credit card to move an existing high-interest credit card balance to a lower-interest card. Doing this will help save you money on interest, especially because many balance transfer cards come with no annual fee and a 0% introductory APR, meaning you don’t have to pay interest for a certain period. Transferring your balance will not only save you money, but it can also help you pay off your credit card debt faster.

The downside is these cards sometimes come with balance transfer fees, transfer limits, and credit score requirements, so a poor credit score may mean you have trouble getting approved. Plus, you should be sure to repay the balance before the intro period is up or face higher interest rates on the outstanding balance.

Learn more: Balance Transfer Credit Cards

Rules of 401(k) withdrawals

Here are some rules and considerations regarding 401(k) withdrawals:

1. Age requirements: Generally, you must be at least 59½ years old to withdraw funds from your 401(k) without incurring a penalty. If you withdraw funds before this age, you may be subject to a 10% early withdrawal penalty in addition to income taxes, unless an exception applies.

2. Required minimum distributions (RMDs): Once you reach age 72 (or 70½ if you reached 70½ before January 1, 2020), you are required to start taking minimum distributions from your 401(k) each year. Failure to take RMDs can result in a 50% penalty on the amount that should have been withdrawn.

3. Employment status: If you are still employed by the company sponsoring the 401(k) plan, you may not be able to withdraw funds from the plan until you reach a certain age or meet other criteria specified by the plan.

4. Hardship withdrawals: In certain situations, such as medical expenses, funeral expenses, or to prevent eviction from your home, you may be able to take a hardship withdrawal from your 401(k). These withdrawals are subject to income tax and, if you are under 59½, the 10% early withdrawal penalty.

5. Tax considerations: Withdrawals from a traditional 401(k) are generally taxed as ordinary income. If you have a Roth 401(k), qualified withdrawals are tax-free.

Note that 401(k) loans are not considered a withdrawal, but rather a loan that must be repaid according to the plan’s terms. Failure to repay the loan could result in taxes and penalties.

Factors to consider when taking out a 401(k) loan

Whether you should take out a 401(k) loan depends on several factors, such as:

- What type of debt it is (such as loans or credit cards)

- How much debt you have and how much you want to borrow

- The interest rate on your current debt and the rate you’ll pay on the loan

- The rate of return you expect on your investments

- How long it will take you to pay off the loan

- How many years it will be until you retire.

- Your credit score

- Your employment situation

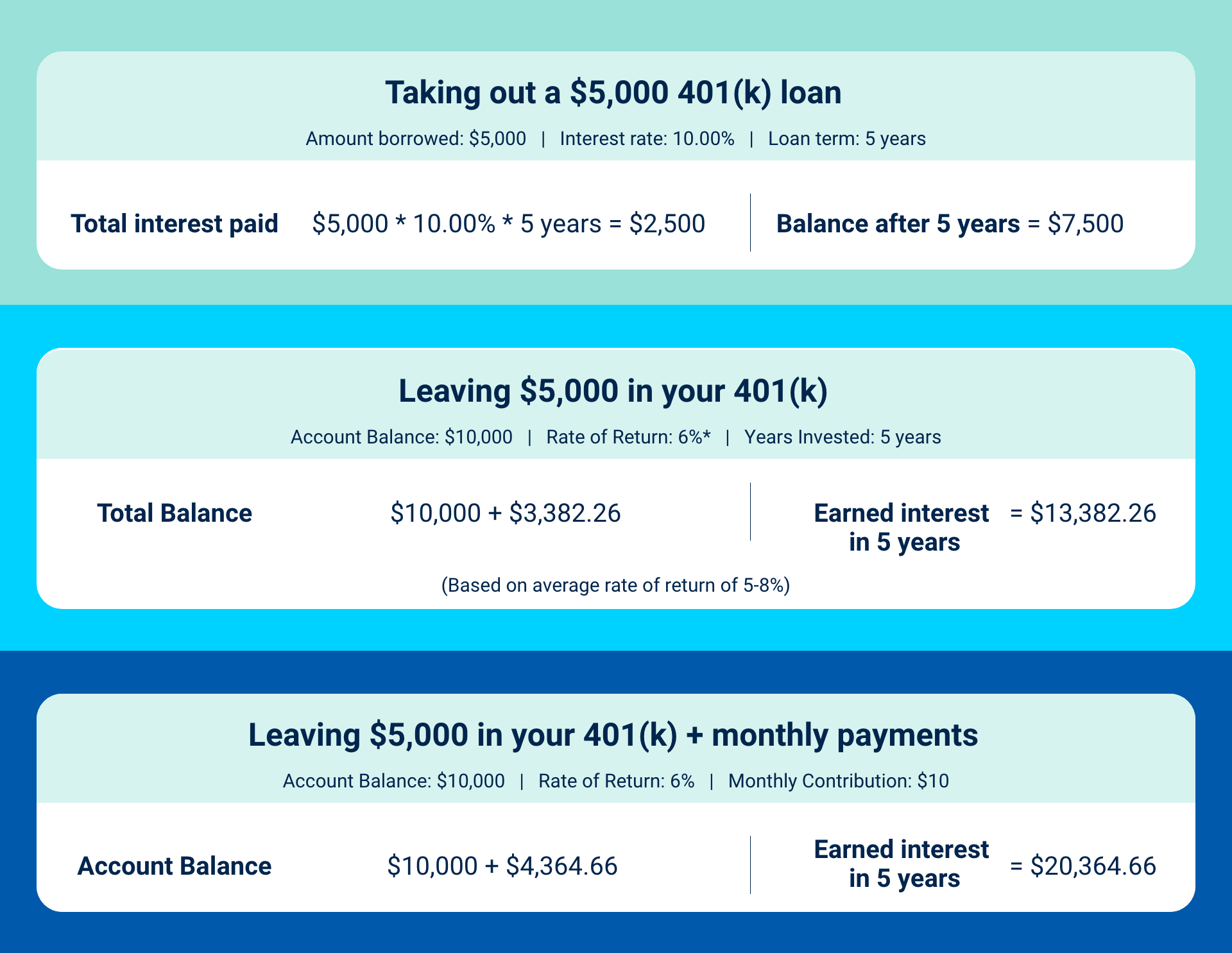

You can decide whether to take out a 401(k) loan or not with the help of this example:

Pros and cons of a 401(k) loan to pay off debt

Pros

1. Can pay off debt faster and save on interest

As we mentioned above, taking out a loan from your 401(k) plan is essentially borrowing your own money. You won’t need to go through an approval process with a lender to borrow the money. If you set up online access, there’s likely an option on the website to do this quickly and conveniently. That’s both good and bad, but we’ll keep it in the “pro” category.

2. Flexible repayment options

Fund administrators want you to pay back your 401(k) loan quickly and painlessly, so they offer flexible repayment options. There are no early repayment fees, and you can set up direct debits to ensure you don’t miss a payment.

3. Low or non-existent lending costs

You may be charged a small origination fee and there might be an administrative charge, but 401(k) loans are the lowest cost lending vehicle you’ll find. If you must borrow to pay off debt, this is likely the best option.

4. Neutral impact on retirement

A common misconception is that borrowing from your 401(k) will have a negative impact on your retirement fund. However, this only happens if you do so during a “bull market,” which is when the market is consistently rising. Otherwise, the impact is closer to neutral, because you pay the money back with interest.

Cons

1. Risk of job loss and quick repayment

No job is guaranteed to be secure. If you lose your job while you still owe money on a 401(k) loan, the IRS requires you to pay off the remaining balance within sixty days. Failing to do that will reclassify the loan as an early withdrawal and you’ll be subject to a 10% fee and income taxes.

2. Could lose investment return

The timing for a 401(k) loan should be carefully considered, especially, if you invest in stock indexes, such as the S&P 500. For example, in 2023, the S&P 500 is up nearly 10%. So, taking funds from your retirement account may not be the best option.

3. Defaulted loans are subject to taxes and penalties

If the loan is not repaid on time, you may owe taxes on the amount you withdrew and a 10% early withdrawal penalty. Unlike the interest repaid on a 401(k) loan, these fees and penalties would not go back into your account. This can quickly add to your debt.

4. May not be able to contribute

In some cases, you may not be able to contribute to your 401(k) while you have the loan out. Not only does this mean missed opportunity for earnings on investment, but you’ll also miss out on any contribution matches provided by your employer. If you repay your loan quickly you won’t lose much, but it could be a disadvantage.

Bottom line

Overall, using a 401(k) loan to consolidate your credit card debt is a huge risk. If you’ve exhausted all other options, you might consider it. However, you risk paying unnecessary taxes and fees should you default, and you sacrifice your retirement savings and peace of mind in the process. Plus, 401(k) loans do not help you stay out of debt because they don’t address the reason you may be in debt in the first place.

FAQs

No, there’s no credit check to qualify for a 401(k) loan, and credit reporting agencies don’t use your retirement savings as a variable when they calculate your credit score.

In most circumstances, a 401(k) loan will not affect your tax return. If you lose your job and can’t repay the loan, the IRS may reclassify it as an early withdrawal and tax you on it.

It’s your money. No one will charge you a fee to borrow it, as long as you pay it back.

No. In most cases, it’s a good idea to take a 401(k) loan to pay off debt because it’s the lowest-cost lending option you’ll find, and you can typically use it to pay off debt fast. Just don’t do it during a bull market or if you think you’ll lose your job soon.

Most plans have a borrowing limit of $50,000 or 50% of the account funds, whichever is less. Plans also typically have a limit on how many loans you can take out at one time.

Though 401(k) loans can come with lower interest rates and no credit checks, they put you at a high risk of paying unnecessary taxes and penalties, not to mention cutting into your retirement savings. Learn about other debt consolidation methods.

If you need the money fast for a short-term expense and can pay back the loan on time, borrowing from your 401(k) is fine. It can be especially effective for your retirement savings if you take out the loan while the stock market is weak. We would not recommend a 401(k) loan for debt consolidation, though.

You can generally withdraw from your 401(k) without penalties once you reach age 59½. This is known as a “normal” or “regular” distribution. You can also take out a 401(k) loan, which is not considered a withdrawal but rather a loan that must be repaid.

Similar to a 401(k) loan, there are pros and cons to using an IRA to pay off debt. This withdrawal would not be considered a loan, so you’d be subject to tax penalties on the amount you withdraw. You may also face additional withdrawal penalties, and you’ll lose out on the earning potential the investment could have had.